Over the last 12 – 15 months of equity market journey, I see a mixed feeling among the investors. Many investors are unhappy with the equity returns. “I’m not making money” or “My returns are negative” is a line I hear often. And some people even feel that they would have been better off with fixed return products. On the other hand, despite the similar experience, there’s an equally vocal group with an investing experience of JUST last 4 to 5 years, willing to defy principles of financial planning. They are contemplating shifting their planned low-risk allocations to high-risk assets like equity – or even gold – merely because of recent outperformance.

For any investor, the goal is simple: make money from money. However, achieving this requires financial planning, asset allocation and investment discipline. And in both the extremes mentioned above, one core principle being ignored is — asset allocation discipline.

I’ve observed this frequently in many of my client conversations. Portfolios are carefully constructed with combination of products based on the suitability of their short-, medium- and long-term goals. This usually means, choosing low-risk low-return products like FD, Liquid Funds or Arbitrage funds for the short-term needs, moderate risk products like Dynamic Asset Allocation Funds or debt funds for the medium-term goals and high-risk high return products like equity funds, multi-asset allocation funds and gold funds for the long-term wealth creation. In short, we invest in the most suitable combination of asset class to ensure a balance of stability and growth. This structure isn’t accidental — it is thoughtfully designed to match the investor’s financial goals in line with the time horizon of each goal. This approach helps the investors to take the calculated risks necessary to achieve the rate of returns required to accomplish the goals efficiently.

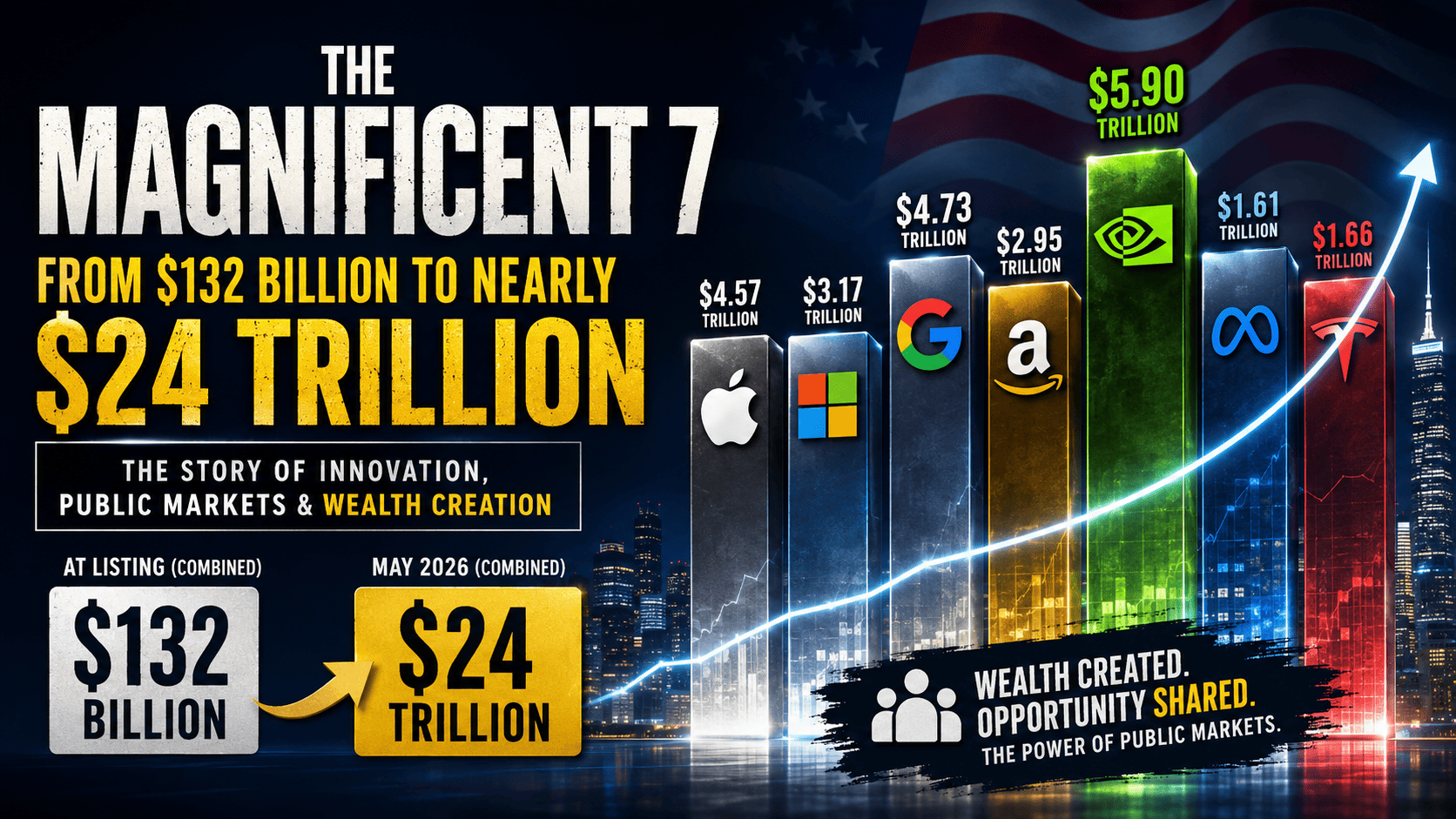

But a lot depends on the initial conversation between the financial advisor/mutual fund distributor and the client. The core idea of investing in mutual funds is to achieve a combination of growth and wealth preservation. This means, the aim is to earn around 2% over and above the nominal GDP (which captures inflation also). Unless explicitly told to take a very aggressive approach (with higher small and mid-cap allocation), the suggested portfolio often tilts a little towards the large cap. Globally too, most financial plans are generally heavy on large cap (as high as 60-70%). Interestingly, the “Magnificent Seven” — the heavyweights of U.S. large caps — have done exceptionally well recently compared to the broader market. India, however, has seen the opposite trend, with large caps underperforming the broader market.

Post covid-19 slump, the capital market experienced an irrational exuberance that has resulted in an exceptional performance of equity-oriented funds. This has created overconfidence and unrealistic expectations, majorly among the new set of investors. Those who (by luck) had significant allocations to mid and small cap funds saw returns of 18%+ (despite last 12 – 15 months underperformance) whereas the large caps have seen a lower double-digit returns. As a natural trait of human behaviour, we tend to register in our minds, the latest best performing asset class be it Gold, Real Estate or Equities (and in this case, small and midcap over large cap). Due to this, lot of investors today believe that this trend will continue indefinitely, that equity is the only asset class worth owning, and mid & small caps are the only way to make money. The surprising (and concerning) trend is that some investors are even willing to shift their long-term debt allocation to equity, purely because recent returns look attractive — despite current valuations.

This is where most investors go wrong. As the saying goes, the wrong decisions are often taken during the best times. Wealth is created not just by participating in markets, but by sticking to the process — disciplined financial planning, goal-based investing and maintaining the right asset mix. Asset allocation should change only when your cash flows, income levels or life goals change — not just because one asset class seems to have done extremely well in the recent past.

Not to forget, we are still in a period of significant uncertainty — whether it’s the US tariff or ongoing Russia–Ukraine conflict, the Israel–Hamas tensions, or the rising friction between China and Japan over Taiwan. The tariff-related disruptions are highest for Bharat. Domestically, food inflation is currently negative, which simply means that the next year’s food inflation could appear higher due lower base effect. At the same time, people are seeing the benefits of GST reforms, lower interest component in an EMI and have more money in their hands due to the new personal tax regime. The macro indicators such as inflation, GDP growth, current account deficit and fiscal deficit remain in India’s favour. However, the market seems to have captured all these in the current valuations.

In such an environment, shifting everything to the present “best-performing” asset class or rushing to move from a low-performing fund into the recent star performer can be risky and counterproductive. In uncertain phases like these, the smartest approach is to remain disciplined. Maintaining a balanced asset allocation, sticking to your financial plan and taking profits periodically (when appropriate) is often the most rewarding long-term strategy.

For long-term financial wellbeing, discipline matters far more than near term excitement.

Shreedhara is the Founder & Director of Ara Financial Services Pvt. Ltd. He has an experience of over 2 decades in Financial Service Industry with majority of it in guiding individuals and institutions on their investments requirements.