As life stages evolve, financial priorities also change. Many individuals explore financial concepts differently after starting a family, especially when planning for education and long-term responsibilities.

I have a client, a young couple who has been with us for over five years, investing with us since they were married. Recently, they came in for a portfolio review since they were expecting their first child.

As we reworked their financial plan together, they were surprised by how much had changed. What was once a plan built around just the two of them now looks very different. Their short-term goals now include daycare expenses, their medium-term goals cover the initial school admission costs, and their long-term goals have expanded to include higher education planning.

It made us reflect on how financial planning for couples with kids can be far more complex and unpredictable than we often assume.

Creating a smart investment plan for couples with kids is one of the most important financial decisions. With aspects of education, healthcare and life goals, raising children comes with increasing expenses. A well-structured investment strategy for parents ensures that your child’s future is secure while maintaining your financial stability.

Why Parents Need a Dedicated Investment Plan

Managing expenses related to education, healthcare, and long-term goals often requires a structured understanding of financial concepts.

This helps in:

- Managing rising costs

- Maintaining financial stability

- Planning for long-term goals

Step 1 – Define Financial Goals for Your Child

- Short-term goals: school fees, extracurricular activities

- Medium-term goals: skill development courses

- Long-term goals: higher education, marriage

Step 2 – Build an Emergency Fund

Maintaining 6–12 months of Income as an emergency fund supports financial stability.

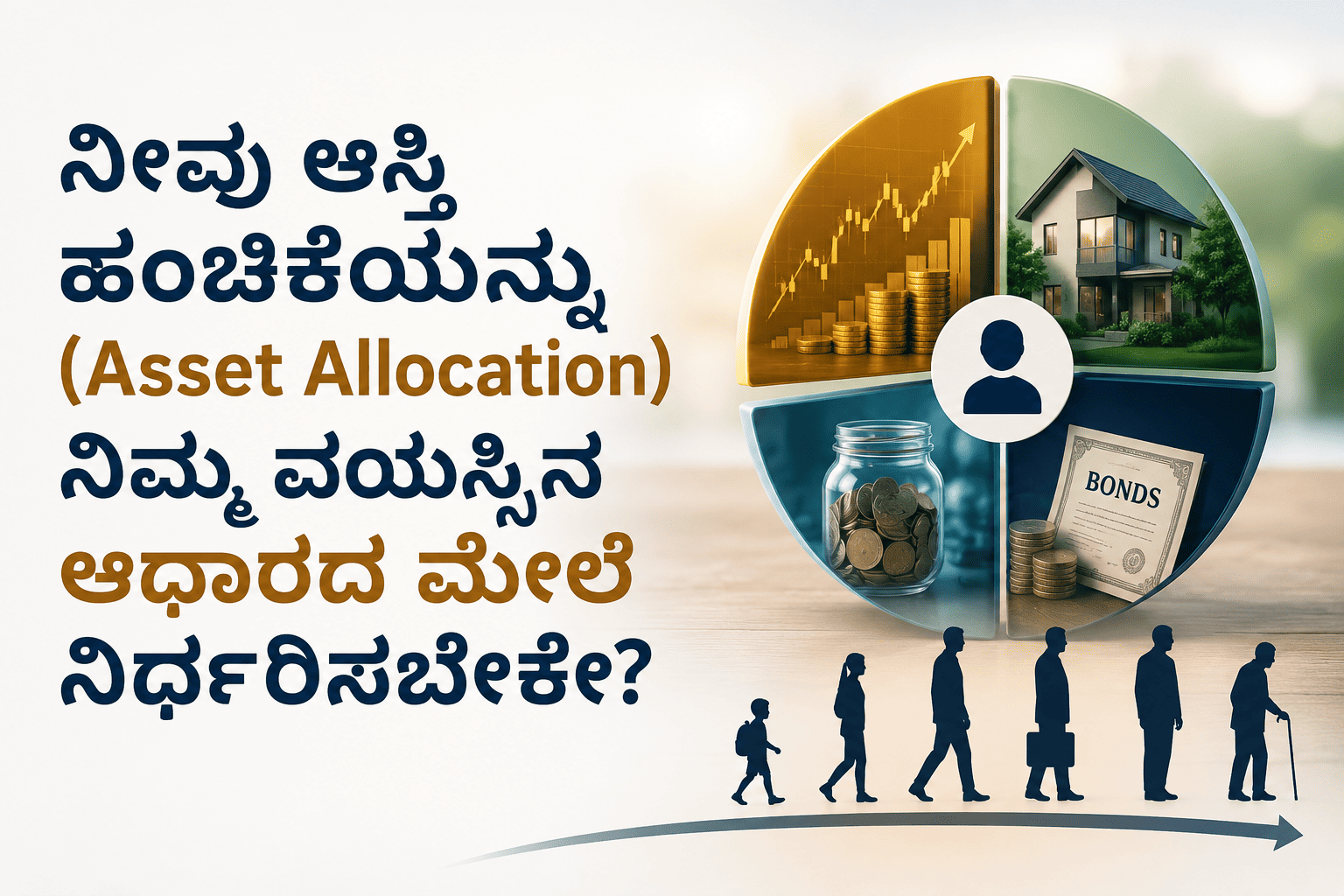

Step 3 – Choose the Right Investment Options

A diversified approach is key to a successful investment plan for parents with kids. Consider these options:

- Equity Mutual Funds, Gold Funds, Multi Asser Funds: Ideal for long-term goals like education

- Fixed Deposits or arbitrage funds or liquid funds: Provide stability for short-term goals

- Hybrid funds are ideal for medium term goals

Step 4 – Start Early for Maximum Benefits

The earlier you start your investment plan for your child, the greater the advantage of compounding. Even small, consistent investments can grow significantly over time, reducing the financial burden later.

Step 5 – Role of Insurance

A comprehensive financial planning for parents must include:

- Term Life insurance to secure your child’s future in your absence

- Health insurance to protect against medical expenses

Insurance ensures that your investment plan remains intact during uncertainties.

Common Mistakes

- Delaying investments

- Ignoring inflation in education costs

- Over-investing in low-return instruments

- Withdrawing from child’s investment for personal expenses

- Not reviewing the plan regularly

Final Thoughts :

Understanding financial concepts, starting early and maintaining consistency can help individuals better navigate financial responsibilities over time.

Disclaimer: This article is published by Ara Financial Services Pvt. Ltd. (ARN-76035), an AMFI-registered Mutual Fund Distributor, for investor education and general informational purposes only. It is not investment advice or a recommendation to buy, sell or hold any investment product. Mutual Fund investments are subject to market risks, read all scheme related documents carefully. Please consult your financial and tax advisors before making any investment decision.

FAQ’s:

Financial awareness helps parents understand how different financial responsibilities, such as education and healthcare, can be approached over time.

Starting when your child is born, is often the best time to start. Many individuals explore investment approaches early to better understand long-term financial concepts related to their child’s future.

Parents should invest in a combination of Diversified Equity Mutual Funds, Gold Funds, Multi-Asset Funds, Index Funds via SIP mode for child's long-term goals.

A Systematic Investment Plan (SIP) helps in long-term investing by enabling regular, disciplined contributions to mutual funds. It benefits investors through rupee cost averaging, which reduces the impact of market fluctuations, and the power of compounding, which accelerates wealth growth over time. SIPs also make investing more accessible and consistent, helping individuals stay committed to their financial goals.

Yes, insurance is an essential part of financial planning as it protects you and your family from unexpected risks. While investments focus on wealth creation, insurance ensures financial security during unforeseen events. It’s important not to mix insurance and investments—opt for pure protection plans rather than combining both objectives. Additionally, having adequate health insurance is crucial, as it helps cover medical expenses and prevents emergencies from causing a significant financial burden or draining your savings.

Shreedhara is the Founder & Director of Ara Financial Services Pvt. Ltd. He has an experience of over 2 decades in Financial Service Industry with majority of it in guiding individuals and institutions on their investments requirements.