Whenever markets fall, there’s a rush of thoughts in our mind. It’s natural because where our hard-earned money is invested, our emotions inevitably follow. In those moments, the urge to act or react becomes strong, often making us lose sight of why we invested in the first place.

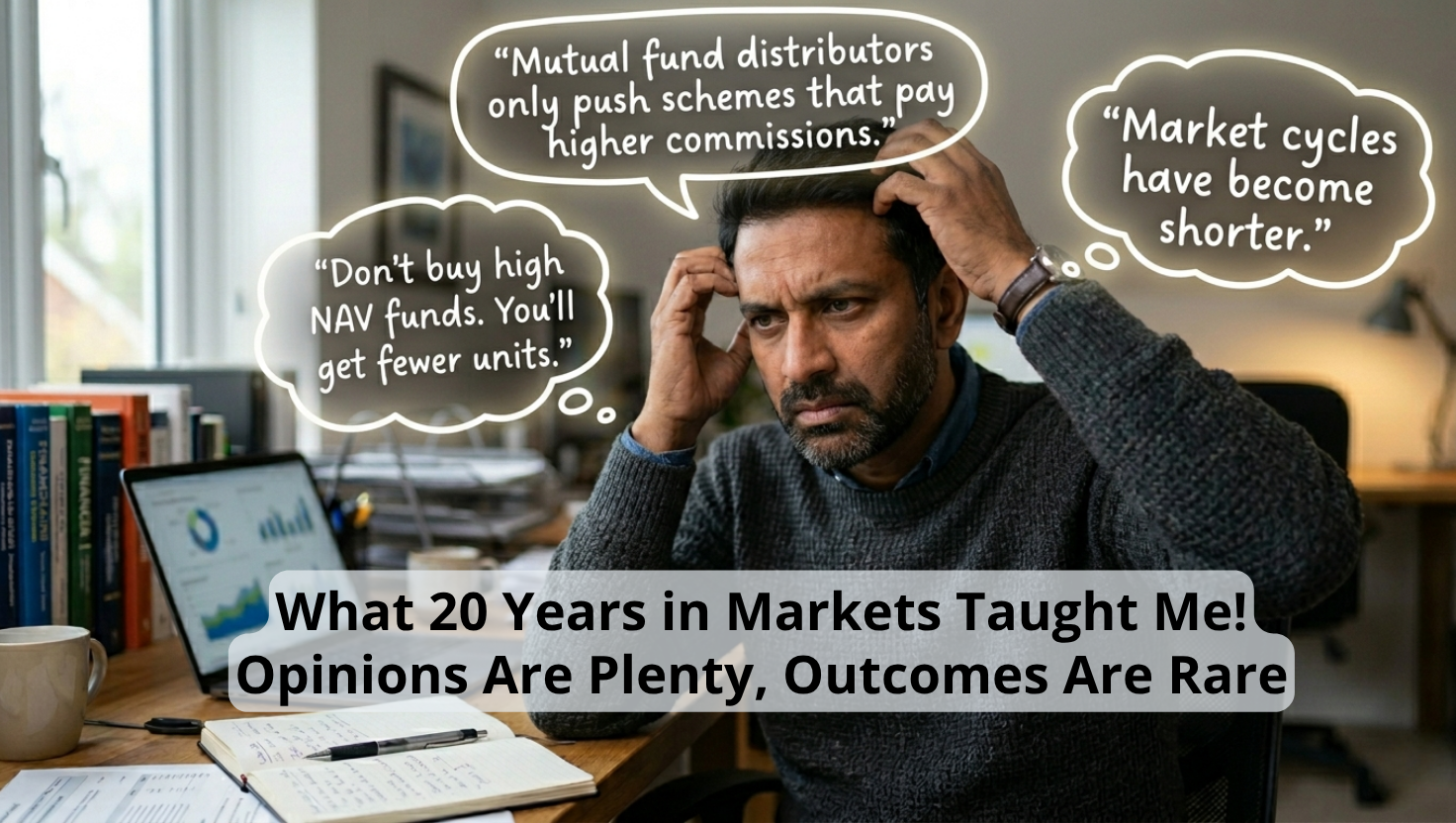

Over the years in this industry, I’ve observed that strong opinions are everywhere, but consistent outcomes are rare. These opinions travel fast in conference stages, WhatsApp groups, office coffee breaks, family dinner tables, news channels, social media, TV anchors/journalists, and financial influencers. Each narrative may sound convincing in isolation, but as investors, we rarely pause to ask: how does this impact my goals?

Things We’ve Heard Over the Years

Here’s a snapshot of what I’ve heard over 20 years in this industry across market cycles, conversations, and investor behaviour:

- “Don’t buy high NAV funds. You’ll get fewer units.”

A classic misconception that confuses unit count with actual wealth creation. - “Higher NAV funds will find difficult to grow.”

Again a misconception where investors doubt that an NAV ₹ 10 can easily grow to ₹ 12 but a ₹ 500 NAV will find it harder grow to ₹ 600. However, they forget the fact that the returns are generated by the underlying market. So, if the market gives 15% return, the funds in similar category will also deliver returns around that range (plus or minus few points depending on which fund was lucky enough to pick the best set of stocks & sector combination for that period) - “Growth at any price is the best strategy.”

A phase where valuations stopped mattering until they suddenly did. When the markets seem bullish, investors often tend to ignore the valuations (I see this often as a sort of FOMO than a mature argument). - “If there is growth, price doesn’t matter. If there is no growth, there is no price.”

Sounds philosophical, but markets eventually bring everything back to valuation discipline. - “Is there any real value in value investing anymore?”

Every cycle makes one style look obsolete, but just temporarily. Markets move in cycles. Some cycles support growth style of investing, some favour value investing. - “PMS is superior to mutual funds.”

Often stated with conviction, rarely evaluated with risk-adjusted data. I have observed that good timing is an important factor in fetching superior returns (risk vs return) when investing via PMS. - “Mutual fund distributors only push schemes that pay higher commissions.”

A perception that ignores the role of advice, suitability, and long-term relationships. Though there can be outliers, but generalising such statements often can be a biased opinion. - “Avoid funds with large AUM. They are too big to outperform.” Several of the most widely marketed funds in the country carry sizeable AUMs and are sold precisely on the back of their track record. Fund size matters, but it matters differently depending on the category, the mandate, and what the fund is actually trying to do.

- “This fund manager is exceptional. He will deliver.” The fund manager matters, of course. But what matters more is whether the fund house runs a robust investment process that holds its shape regardless of who is sitting in the chair. A process-driven fund can survive a manager change. A personality-driven fund often cannot. Following a person is a reasonable starting point. Making it the entire thesis is where it gets fragile.

- “FIIs are selling while Indians are buying. Something must be wrong which we aren’t able to see.” Narratives get built around flows, but outcomes depend on fundamentals and time. Though for decades, FIIs have been the major investors but this trend has been changing fast in India.

- “Emerging markets are far riskier than developed markets.”

A statement that needs constant re-evaluation in a world where macro dynamics have been shifting. - “Market cycles have become shorter.”

Yet, corrections still test patience longer than most investors expect. What matters is how best investors can stay aligned to their goals rather than reacting to every market cycle. - “Markets haven’t made money for the last 18 months.”

Whether 18 months is short or long depends more on investor expectations than market reality. In the long term, these dips help in creating the best wealth and make the portfolio stronger. - “Switch from Scheme A to Scheme B as it is performing well now.”

Performance chasing dressed up as smart decision-making. Switching between schemes (either from a Flexicap to Flexicap or a Flexicap to mid/small cap) may feel very logical but often can be an irrational decision. It is important to maintain a balance between large, mid and small cap along with the mix of growth as well as value style of investing. This gives a reasonable balance to the portfolio to weather through different market cycles. - “Freshers should create alternative income sources early.”

Often at the cost of investing in their primary skill and earning potential. This is a stage of career growth and wealth accumulation using the primary source of income – job/profession. This may hardly add any value and also dilute wealth creation. - “Invest in mutual funds for 18% returns and set an SWP (Systematic Withdrawal Plan) of 10% for regular monthly income.”

A clear mismatch between return expectations and sustainable withdrawal rates. Historical data on long term returns clearly suggest that this expectation is far away from reality. Planning this with the help of a mutual fund distributor or an advisor can help you align your expectations and have a practical approach. - “Buy good stocks, hold them for the long term and wealth is guaranteed.”

Even fundamentally strong stocks can stay stagnant for years. This should not be the major source of wealth creation plan for today’s investor. - “Invest in trending sectoral/thematic funds like defence or manufacturing.”

If the theme is popular and most talked about, much of the upside is already priced in. One needs to be ahead of the trend to make superior returns which is often impossible. May not be suitable for someone investing as part of goal planning. - “Move emergency funds to high-return bonds as FDs & Liquid Funds don’t pay enough.”

Optimising returns is not bad, but greed is the first step for a bad financial decision. Ignoring liquidity and safety for marginally higher returns can defeat the very purpose of having an emergency fund. - “Spend 1 hour a day for trading and earn a steady income.”

Underestimating the skill, discipline, and risk involved in trading. If the intent is to grow money, then risking it to a strategy where success ratio is low can be disastrous. Products like mutual funds have a proven track record of long-term wealth creation. Use them for growth and spend quality time to enhance your expertise which can help you grow in your career and support long term wealth creation.

What Actually Lies in Your Control

None of the narratives above are the ingredients that build wealth. They are the noise around it.

In life, even job security, for example, isn’t fully in your control. What is in your control is how you show up, how consistently you work, and how you respond to uncertainty.

Investing is no different.

As an investor, most of what drives markets, like interest rates, global flows, geopolitics, economic cycles, corporate performance, is outside your control.

What is in your hands:

- Following a disciplined investment approach

- Staying consistent across market cycles

- Avoiding reactionary decisions based on noise

- Building a well-diversified portfolio across asset classes

- Aligning investments with your time horizon and goals

Markets will always be filled with opinions. Your success depends on whether you have a process.

Shreedhara is the Founder & Director of Ara Financial Services Pvt. Ltd. He has an experience of over 2 decades in Financial Service Industry with majority of it in guiding individuals and institutions on their investments requirements.