One of the first few questions investors usually ask after completing the basic formalities like KYC and account opening on the NSE platform is either “Which mutual fund is the best to invest in now?”, “Which fund is performing well?” , “Should I invest a lump sum now?”, “Should I wait before starting my SIP?”, “Should I go for STP?” or “How can I make the best use of STP to get good returns?”

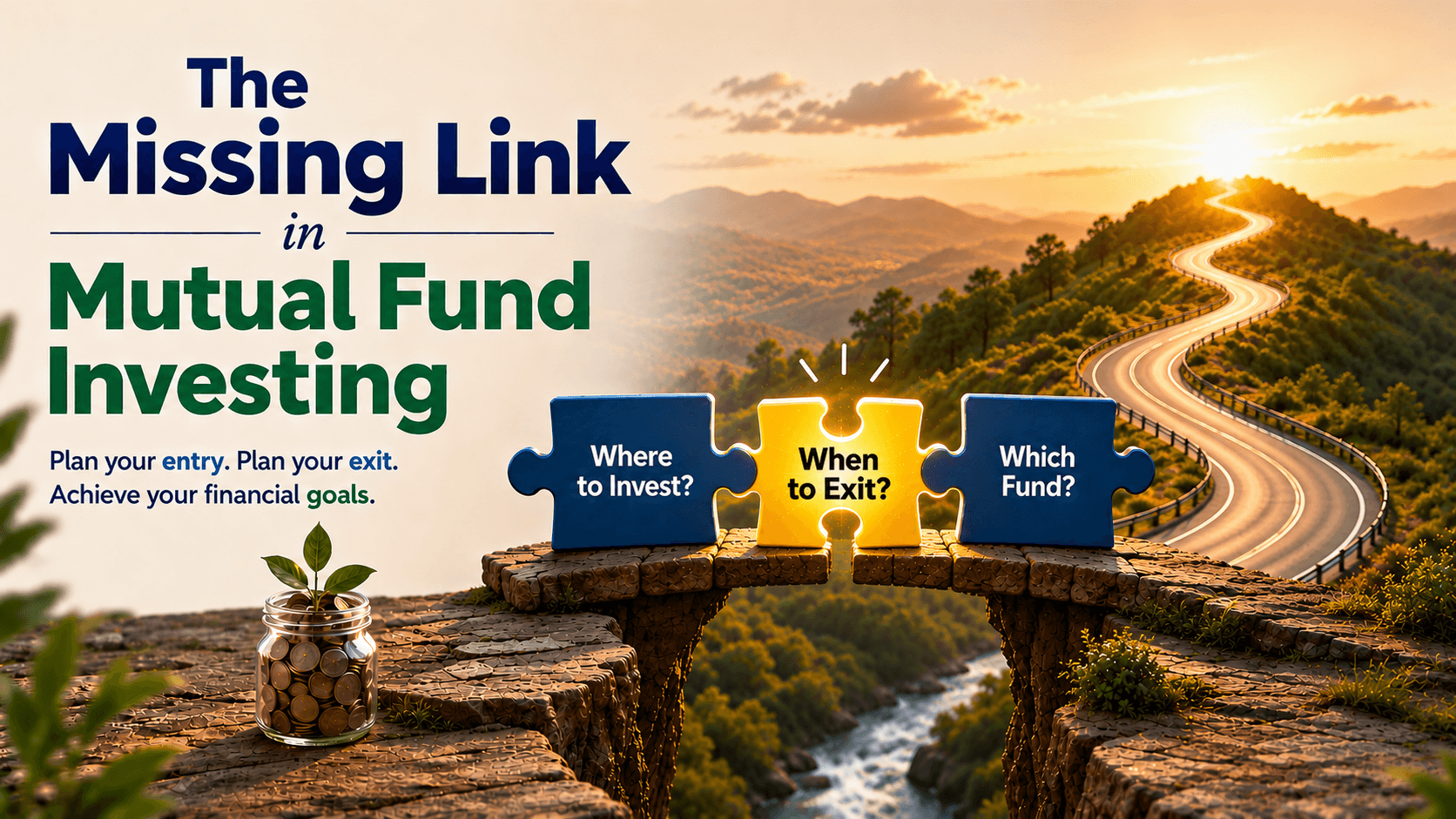

In general, most investors spend a significant amount of time thinking about where to invest, when to enter, and which fund is best. But in my experience, one equally important aspect of investing that often gets very little attention is when to exit a mutual fund investment.

That becomes the missing link in mutual fund investing in many cases.

Why do people invest

Broadly speaking, people invest for two reasons:

- To achieve specific financial goals

- To create long-term wealth

The products, the asset class, and the rationale for buying and holding investments may be the same for both reasons. However, the reason and approach to exit the investment differ substantially.

Exiting When Investing for a Financial Goal

Every financial goal comes with a timeline. Education, retirement, marriage, buying a home, international travel, or changing a vehicle, or any such goals, have a target period attached to them.

Let us take education planning for your young child as an example.

We understand that the larger expenses for education generally begin during Plus Two, graduation, and post-graduation. If parents aspire to send their children abroad for higher education, get admission to a premier institution, or pursue a specialized course, the financial plan must be designed accordingly for a larger corpus.

In most families, school expenses till the 10th standard are managed using regular income because parents are usually actively earning then. Some parents additionally maintain SIPs in a liquid fund, an arbitrage fund, and some even have a recurring deposit in their banks to manage annual school fee payments comfortably.

In general, the largest expenses towards children’s education start between the ages of 15 and 20, covering Plus 2, graduation, and post-graduation. Since these costs are likely to be much higher in the future, parents should plan by estimating what education may cost when their child turns 16, 17, or 18. They should build an investment strategy today that is aligned with tomorrow’s financial needs.

The investor should keep track of the timelines of their goals and should start thinking of finances well in advance. Ideally, they should review their portfolio at least one or two years before the goal arrives. During this phase, your financial advisor proactively discusses the present market dynamics, which will help you shift a portion of your investment from growth-oriented assets to safe assets so that the accumulated corpus is safe from market volatility.

The same principle applies to retirement planning, marriage goals, travel plans, vehicle replacement, post-graduation plans, and any other major long-term financial goals.

In goal-based investing, timely and disciplined withdrawal planning is equally important as planning for investment in the correct products.

Investors should monitor the performance of the scheme, changes in the fund’s investment style or attributes, and whether the scheme still suits the original financial plan. This may sometimes lead to the reshuffling of the schemes within the portfolio to ensure the investments remain aligned with the financial plan. Although this technically involves exiting one scheme and entering another, it should not be confused with goal-based redemption. Rebalancing is part of portfolio management, not necessarily an exit from investing itself.

At Ara Financial Services, we have been efficiently helping investors achieve their financial goals for over 20 years. We understand the investor’s life stage, financial goals, cash flow requirements, risk profile, and investment horizon, and then suggest a bunch of products best suited for them. We conduct periodic portfolio reviews, monitor progress against timelines, and make adjustment whenever necessary to keep the investor on track toward their goals. This helps investors in 2 ways: One, in preventing emotional decision-making during periods of market volatility, and two, in planning their withdrawals well in advance rather than waiting until the last moment to redeem their investments.

Exiting When Investing for Wealth Creation

Consider investors who are investing primarily for long-term wealth creation. These are affluent investors who have structured their portfolios across multiple asset classes, ensuring that both their cash flow requirements and wealth creation goals are addressed.

In such cases, there may not be a predefined exit timeline. If the portfolio is well-constructed and continues to remain aligned with the investor’s objectives, there may be no reason to exit frequently. Long-term wealth creation often requires patience, discipline, and the ability to stay invested through multiple market cycles.

When Does Exiting a Mutual Fund Make Sense?

There is no universal rule that applies to every investor, but exits are generally justified in the following situations:

1. When the Financial Goal is Reached

If the purpose of the investment has been fulfilled, the money should now serve its intended purpose.

2. When Asset Allocation Changes

Sometimes one asset class grows disproportionately and increases portfolio risk. Rebalancing may require partial redemption.

3. When Life Circumstances Change

Changes in income, responsibilities, career, health, or financial priorities may require a revised investment strategy.

4. When a Fund Consistently Underperforms

Every fund can go through temporary underperformance. However, if a scheme continuously lags behind peers and benchmarks over a meaningful period, it may require review or replacement.

Investing is a Journey with a Destination

Most investors begin their journey with a financial goal in mind. The investment starts with a purpose, a timeline, and an expected outcome. Ideally, both entry and exit should be planned around that goal. But what we have seen is, over time, many investors drift away from their original plan because of market narratives such as “Markets are falling, you should withdraw,” “This scheme is not performing well,” and “Everyone is moving to another asset class.”

But investing and redemption should not be done randomly. Think of it like a journey. You do not board a train without knowing where you want to go. Similarly, every investment should have a strong answer to “why you are investing,” “how long you are investing,” “what role the investment plays,” and “when and how you may eventually withdraw.”

Understanding the current valuation, which product to invest in, and how to invest (to invest lumpsum or through STP) is crucial when the investment is one-time. But equally important is the rationale behind redemption. We should carefully consider when to exit, what to do with the money we get after redemption, and how to manage the tax implications of withdrawal.

Political events, geopolitical tensions, economic cycles, environmental disruptions, and war-like situations will continue to influence markets. Portfolios will move up and down through these cycles. That is the nature of markets, and everyone must live with this. Your major investments and redemption decisions should never be based on market volatility.

The next time you invest in a mutual fund, do not limit your decision to where and how much to invest. Give equal importance to when you may exit, the reason for the exit, and how to deploy the redeemed amount thereafter. Thoughtful planning at both ends of the journey can make the difference between merely investing and successfully achieving your financial goals.

Shreedhara is the Founder & Director of Ara Financial Services Pvt. Ltd. He has an experience of over 2 decades in Financial Service Industry with majority of it in guiding individuals and institutions on their investments requirements.