Yesterday, I met a young professional in his late twenties. He has a good job, a growing salary, and an extraordinary commitment to investing.

“I don’t want to waste money,” he told me. “I keep my expenses to the minimum and invest almost everything I can.”

I was impressed!

Then I asked him where he invested this earning.

“Equity mutual funds,” he replied immediately. “I am young. I can take risks. I have at least 25 to 30 years ahead of me. Why should I put money anywhere else?”

He also added that he had heard the advice repeatedly that “when you are young, invest aggressively in equity. Time is on your side.” And he had followed it with absolute discipline.

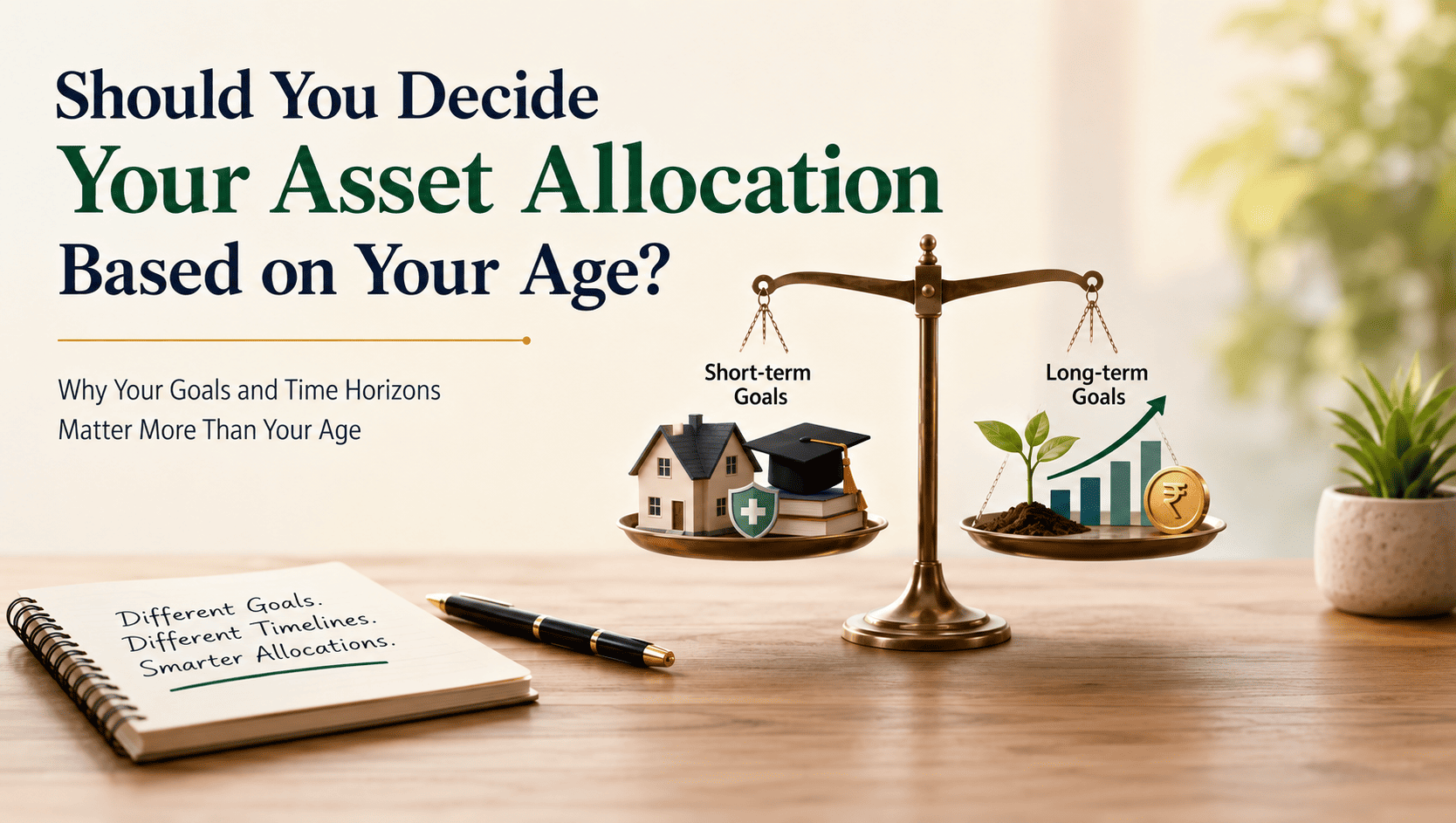

So, what do you think? Is considering age the primary driver of asset allocation the right approach?

The Problem With Age-Based Investing

One of the most common rules in personal finance is simple: when you are young, invest aggressively in equity; as you grow older, steadily move towards fixed income.

This simplicity is attractive, but if you analyse, the reality is more complicated.

Consider a 29-year-old professional with a good salary. Does being young automatically mean that almost all investable money should go into equity?

What if he plans to buy a house in three years? What if he wants to pursue higher education? What about money for an emergency, a career break, or a major family responsibility?

Equity markets can be powerful long-term wealth creators, but they are not predictable over short periods. Money that may be needed in the next few years should not be exposed to excessive market risk simply because the investor is young.

A young age does not make all your goals as long-term goals.

Retirement Does Not Mean the End of Growth

Now consider the opposite situation.

A person retiring at 60 may live until 85, 90, or beyond. That means the retirement corpus may need to support three decades of expenses.

If nearly the entire portfolio is shifted to fixed income before retirement, the investor may reduce short-term volatility risk but may increase the long-term risk of purchasing power loss.

Groceries become more expensive. Healthcare costs rise. Travel costs increase. Household expenses change. A monthly lifestyle costing ₹1 lakh today could require significantly more in the years ahead.

This is why retirement planning should not be viewed as a single end date. At 60, some money may be needed next month, some after five years, and some perhaps only after 15 or 20 years.

Let Goals and Time Horizons Drive Asset Allocation

A more thoughtful approach is to allocate money based on when it will be needed.

Funds required for emergencies and near-term goals should generally be kept in relatively stable and accessible avenues. Medium-term goals need an appropriate balance between growth and stability. Money intended for distant goals may benefit from greater exposure to growth assets, depending on the investor’s risk capacity and circumstances.

This principle applies at every age

A 30-year-old may need conservative investments for a house down payment three years away. A 65-year-old may still need growth-oriented investments for money that will not be touched for another 15 years.

Your age is only one piece of information for financial planning. It should not become your entire investment plan. A robust financial strategy is not about being aggressive when you are young and conservative when you are old. Good financial planning is ensuring that the money you need tomorrow is protected, the money you need decades later continues to grow, and every rupee has a purpose aligned with time.

Coming back to my conversation with young professionals, I asked him a few more questions. “Do you plan to buy a house in the next few years? Any plans to pursue higher education? How can u handle a career break? What if an unexpected family responsibility comes up?”

He did not have answers, so he paused.

He had been investing with remarkable discipline, but he had never stopped to ask a crucial question: What is each investment meant for, and when might I need that money? After a detailed discussion, he began to see the limitation of using age as the primary guide for asset allocation. We are now in the process of building a more thoughtful financial strategy that aligns his investments with his goals, time horizons, liquidity needs, and risk capacity.

Disclaimer: Ara Financial Services Pvt. Ltd. is an AMFI – Registered Mutual Fund Distributor (ARN – 76035). The purpose of this blog is to educate public on topics around personal finance, mutual funds & investing. The scenarios mentioned in the blog are to help readers understand the concept clearly. Do not treat our blogs as investment advice or an invitation/recommendation to invest in mutual funds or capital market or take any investment decision. Ara, its employees or the author cannot be held liable for any investment decisions taken on basis of the information in the above blog/article or any other reasons. Please consult an investment advisor or a mutual fund distributor for all your investment needs.

Shreedhara is the Founder & Director of Ara Financial Services Pvt. Ltd. He has an experience of over 2 decades in Financial Service Industry with majority of it in guiding individuals and institutions on their investments requirements.