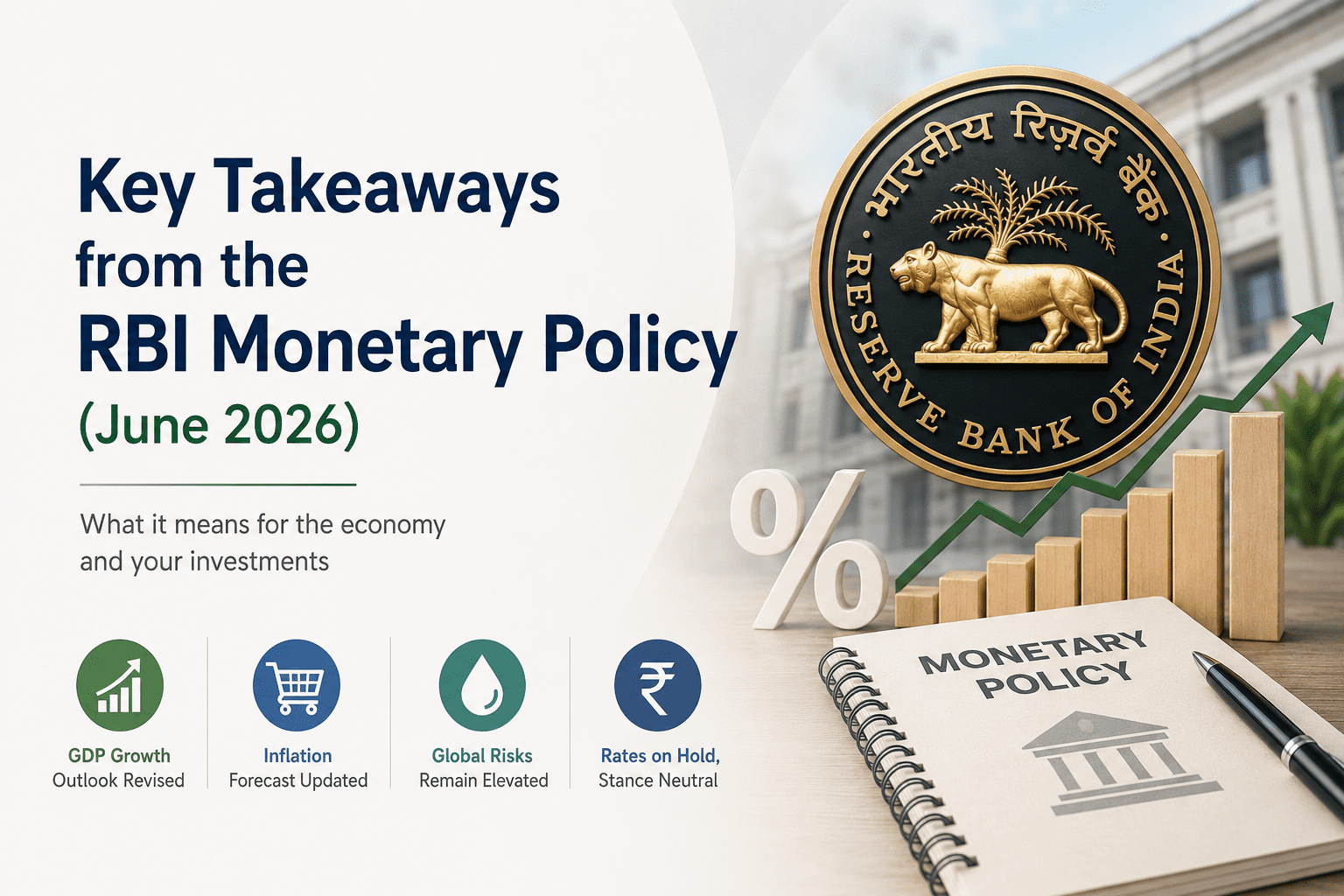

The Reserve Bank of India did today what markets largely expected: it held the repo rate steady at 5.25%. Unanimous. All six members of the Monetary Policy Committee in agreement. The policy stance remains ‘neutral.’

But if you only read the headline, you missed the story.

Behind the decision lies a central bank walking a careful tightrope trying to support an economy that is growing, while watching crude oil prices rise, a monsoon that could disappoint, and a geopolitical storm brewing in West Asia that India cannot fully control. For the long-term retail investor, particularly one invested in mutual funds, today’s announcement has real implications. Let’s break it down.

What the RBI Announced Today — The Key Numbers

- Repo Rate: Unchanged at 5.25% (third consecutive hold; third straight meeting with no change)

- Policy Stance: Neutral – meaning the door remains open in both directions

- FY27 GDP Growth Forecast: Revised downward to 6.6% from 6.9%

- FY27 CPI Inflation Forecast: Revised upward to 5.1% from 4.6%

- Quarterly Inflation Path: Q1 FY27 at 4.2%, rising to 5.1% in Q2, peaking at 5.9% in Q3, and easing slightly to 5.4% in Q4

- Core Inflation: Stable at 3.7%; excluding precious metals, a reassuring 2.1–2.2%

The RBI Governor, Sanjay Malhotra, was measured but candid: global uncertainty driven by the West Asia conflict, elevated crude oil prices, supply chain disruptions, and rupee pressure is real. India entered this period with stronger macroeconomic fundamentals than in past crises. But that does not mean it is immune.

It is worth noting that since February 2025, the RBI has already delivered a cumulative 125 basis points in rate cuts. The current pause is partly about letting those cuts work through the system.

What’s Encouraging for Retail Mutual Fund Investors

Rates are not going up. That is the clearest signal from today. A neutral stance, with inflation still within manageable territory, means there is no case for a rate hike right now. For equity mutual fund investors with long-term SIPs, this matters. Stable rates support corporate borrowing, consumption, and earnings growth – the foundation on which equity valuations rest.

Domestic fundamentals remain intact. The RBI noted that manufacturing and services PMIs continue to show expansion. Rural demand is holding up. MSMEs are resilient. The aggregate story of India’s economy, consumption-driven, services-led, has not changed because of events in West Asia.

Core inflation is benign. Strip out precious metals, and core inflation sits at just 2.1–2.2%. This means the cost pressure in the economy is not broad-based. It is largely energy and food – external and seasonal. For debt mutual fund investors, this keeps medium-term bond yields from spiking sharply and provides reasonable stability in debt fund NAVs.

Liquidity conditions are comfortable. Recent RBI data shows Variable Rate Repo auctions are undersubscribed, a sign that the banking system has adequate liquidity. This supports smooth functioning of the money markets and benefits short-duration and liquid mutual funds.

Where Caution Is Warranted

Inflation is expected to rise through the year. At 5.9% projected for Q3 FY27, India is moving dangerously close to the RBI’s upper tolerance band of 6%. If actual prints come in higher because of a poor monsoon or a crude spike, the RBI’s flexibility to cut rates disappears. For investors parked in long-duration debt funds, this is the key risk: if rates cannot fall, the capital appreciation thesis for long-duration bonds weakens.

The rupee is under pressure. Elevated crude oil prices and global risk-off sentiment are weighing on the rupee. A weaker rupee means imported inflation – pushing up the cost of oil, electronics, and edible oils. The RBI is intervening in the forex market, but sustained rupee depreciation would feed directly into the CPI basket.

The monsoon is uncertain. The RBI explicitly flagged a sub-normal southwest monsoon forecast and El Niño risks. A poor monsoon raises food prices, particularly vegetables and cereals, which form a large share of the Indian inflation basket. This is the most unpredictable variable in the next two quarters.

Geopolitical escalation cannot be ruled out. The West Asia conflict is currently the single biggest external risk. If it spreads to key Gulf oil infrastructure, crude oil prices could move well above current levels triggering a stagflationary shock that no central bank wants to manage.

Factors That Could Force the RBI to Change Course

If any of the following scenarios unfold, the current neutral stance could tilt toward hawkishness – meaning rate cuts go off the table entirely:

- Crude oil sustaining above $95–100 per barrel for two or more months

- A significantly below-normal monsoon leading to persistent food inflation above 8%

- Rupee depreciating sharply beyond the current range, causing material imported inflation

- CPI prints for Q2–Q3 FY27 coming in materially above the 5.5–5.9% projected range

- A major escalation in the West Asia conflict disrupting global supply chains and energy markets

- Fiscal slippage at the central or state level, expanding government borrowing and crowding out private investment

- A reversal in global rate expectations if the US Fed or other major central banks tighten again

Any one of these, individually, might not force the RBI’s hand. Two or three together, arriving simultaneously, would.

What Long-Term Mutual Fund Investors Should Take Away

The big picture is this: India’s economy is growing, rates have fallen significantly from their peaks, and the RBI is watching carefully before moving in either direction. For investors in equity mutual funds through SIPs, this is not a reason to stop or pause. The long-term growth story remains intact.

For debt fund investors, the ideal positioning right now is toward shorter to medium durations. Long-duration bets carry meaningful risk if inflation surprises on the upside in Q2–Q3 FY27.

And across all categories, the most important thing a retail investor can do right now is not react to today’s headline.

Uncertainty is not a reason to exit. It is a reason to stay the course and review the composition of your portfolio with someone who can read these signals with you.

Disclaimer: This article is published by Ara Financial Services Pvt. Ltd. (ARN-76035), an AMFI-registered Mutual Fund Distributor, for investor education and general informational purposes only. It is not investment advice or a recommendation to buy, sell or hold any investment product. Mutual Fund investments are subject to market risks, read all scheme related documents carefully. Please consult your financial and tax advisors before making any investment decision.

Pratik Vora is a Certified Financial Planner and Associate Partner at Ara Financial Services. He has more than two decade’s experience in Banking & Financial Services Industry.