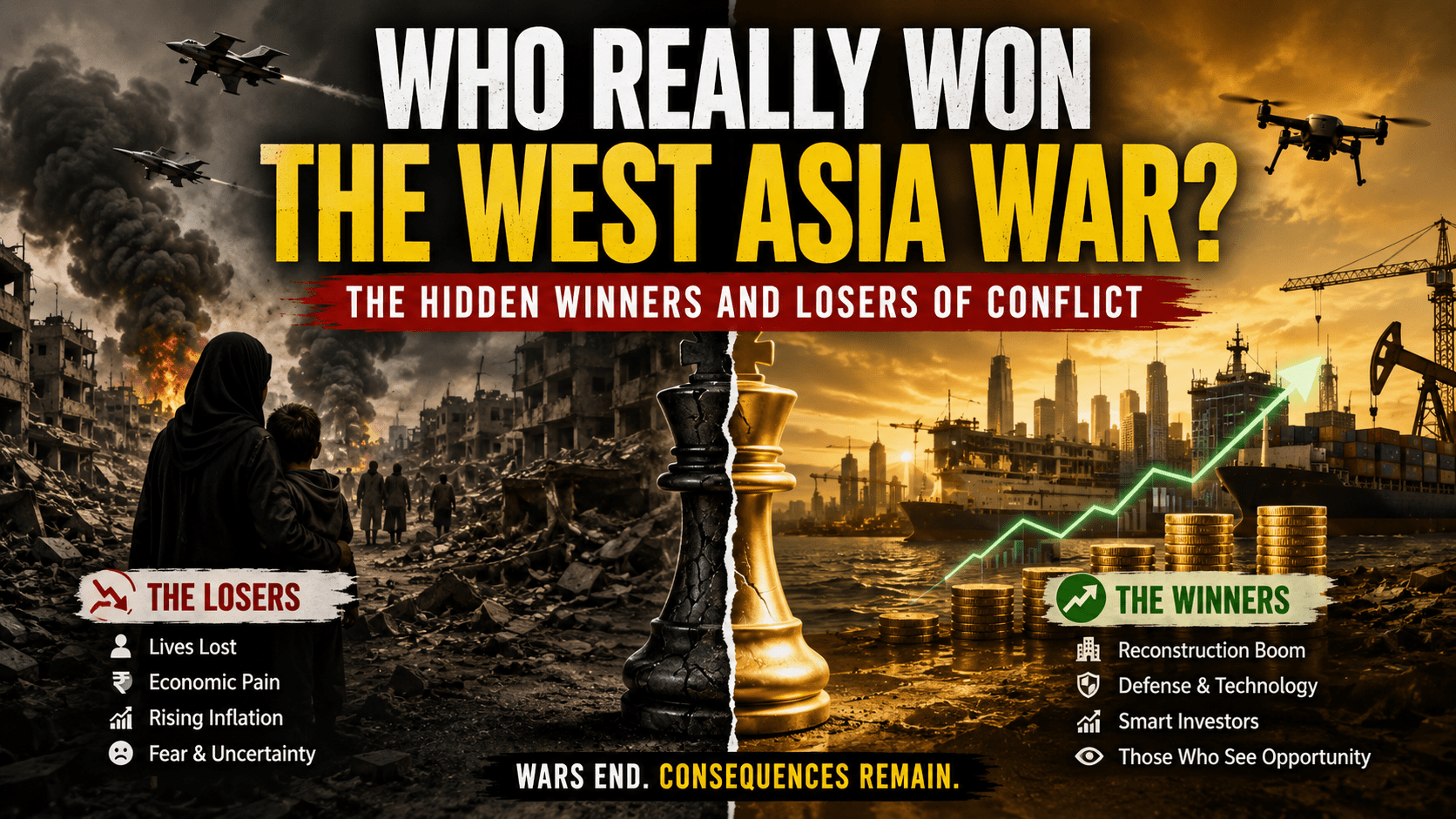

The West Asia war finally appears to be moving toward a ceasefire, with a deal expected to be signed on 19 June 2026. Hopefully, the agreement is actually signed this time and does not become another reminder that in geopolitics, a deal is rarely done when it is announced; it is done when everyone finally runs out of reasons to walk away from it. Geopolitics has a remarkable talent for producing surprises at the eleventh hour. Assuming there are no last-minute surprises, the region may enjoy at least a temporary pause for the next sixty days.

Predictably, the global media has already moved on to its favourite post-war exercise: deciding who won and who lost.

The debate is fascinating because every answer depends on where one stands. A far-right commentator sees one winner. A far-left commentator sees another. The centre-left has its own equations. The centre-right has its own calculations. Experts produce charts, television panels produce noise, and social media produces confidence unsupported by evidence.

But for a common citizen watching events unfold from thousands of kilometres away, perhaps the question is simpler.

Before asking who won, we should first understand who lost.

The Biggest Losers Never Chose the War

The first loser is the ordinary individual who was never part of the decision-making process and yet lost his/her life.

The pilot flying a combat mission, the captain navigating a merchant vessel through increasingly dangerous waters, the crew member on that ship, the truck driver transporting fuel, the engineer maintaining critical infrastructure, and the citizen sitting quietly at home on either side of the conflict – all of them become participants in a war they never chose.

Countless people lost their lives. For strategists, these individuals are often represented by statistics. For families, they are the breadwinners in the form of fathers, mothers, sons, daughters, and spouses.

A geopolitical conflict is discussed in terms of missiles, deterrence, air superiority, and strategic depth. But every war is ultimately paid for by people who never attended the meetings where the decisions were made.

For those advocating war, a life may be just a number. For the family that loses that life, it remains priceless.

The Invisible Casualties: Countries That Did Nothing Wrong

The second set of losers are countries that had absolutely nothing to do with the conflict.

A war in West Asia instantly becomes a tax on energy-importing nations. They do not just import oil and energy; they end up importing pain of inflation along with them.

Countries dependent on imported crude oil suddenly face higher import bills. Foreign exchange reserves come under pressure. Currencies weaken. Fiscal deficits widen. Balance-of-payments calculations become more difficult.

And all this happens despite those countries making no mistake of their own.

Economists often talk about “external shocks.” It is a sophisticated phrase that essentially means: someone else’s problem just became your problem.

For many developing economies, years of careful fiscal planning can be pushed back by three to five years because of events occurring thousands of kilometres away.

That is the frustrating reality of globalization.

The world is interconnected when profits are being made and interconnected when losses are being distributed.

Why India Could Not Afford This Conflict

India is a useful example.

Agriculture contributes roughly 16 –18% of India’s GDP, but more importantly, it supports the livelihood of nearly 45% of the population. Agriculture is also heavily dependent on fertilizers, a sector where India remains significantly dependent on imports for key raw materials and inputs.

Now imagine a year impacted by El Niño conditions, where agricultural stress is already elevated.

Add expensive fertilizer imports, higher shipping costs, rising crude oil prices, and disruptions across critical maritime routes. The result is a significant burden on the country’s finances.

India imports more than 80% of its crude oil requirements. When oil prices rise sharply, the impact does not remain confined to oil companies. It spreads across transportation, manufacturing, agriculture, logistics, and household budgets.

The final bill runs into lakhs of crores.

And unlike corporate earnings reports, the average citizen cannot simply adjust the narrative.

The bill eventually arrives at the petrol pump, the grocery store, the electricity bill, and the monthly household budget.

Inflation’s Cruel Mathematics

Inflation is perhaps the most democratic form of pain.

It reaches everyone. The wealthy feel it, the middle class feels it, and the poor feel it the most.

A family that was able to save ₹10,000 a month may suddenly save ₹7,000. Another family saving ₹5,000 may save only ₹2,000. Some stop saving entirely.

The tragedy of inflation is that it rarely appears dramatic on television screens. There are no breaking-news banners announcing that millions of people have become slightly poorer.

But over time, those small losses compound.

And compounding works both ways.

Albert Einstein may or may not have called compounding the eighth wonder of the world. Inflation certainly behaves as one of its evil cousins.

The Investor Who Lost to Fear

Then there is another category of loser.

The investor. Not because markets fell. But because fear won.

Every geopolitical crisis creates a familiar cycle. News channels predict catastrophe, social media predicts the end of capitalism, and market experts discover fresh reasons why “this time is different.”

And some investors stop their SIPs. Some redeem their mutual funds. Some sell perfectly good businesses because a missile was launched somewhere far away.

History repeatedly shows that markets recover faster than headlines.

The investors who stopped investing because of war may discover years later that the biggest damage to their portfolio was not caused by missiles.

It was caused by panic. Volatility feels dangerous. Abandoning discipline often is.

So, Who Actually Won?

Now comes the uncomfortable part.

Someone always benefits.

Not necessarily because they wanted the war. Not necessarily because they caused the war. But because incentives follow money.

Whatever gets destroyed must eventually be rebuilt. Roads, ports, power infrastructure, oil fields, refineries, fuel distribution networks, gas facilities, industrial plants, transportation systems, defence assets, and communication infrastructure all need to be restored or rebuilt.

The companies involved in reconstruction become the first-round beneficiaries. Capital goods companies, engineering firms, infrastructure contractors, defence manufacturers, drone producers, and technology suppliers are likely to see increased demand as reconstruction spending gathers pace.

Their order books grow. Their revenues expand. Their shareholders benefit. Their promoters benefit. Dividend recipients benefit.

This is not a moral judgment. It is simply how economics works. Destruction creates reconstruction demand. Reconstruction creates economic activity. Economic activity creates profits. And profits find shareholders.

Crisis: The World’s Most Reliable Wealth Transfer Mechanism

There is another winner. The disciplined investor.

The individual who continued investing despite frightening headlines accumulated more units at lower prices.

When markets eventually stabilize, those accumulated units become valuable.

The irony is striking. The same event that creates fear for one investor creates opportunity for another. The difference is often not intelligence. It is temperament.

As Morgan Housel frequently reminds us, investing success is less about what you know and more about how you behave.

Information: The Most Valuable Asset During War

Then there are those who profit from information.

Or perhaps from being closer to information.

Markets now react to every speech, every diplomatic leak, every military statement, and sometimes every social media post.

A single post on Truth Social can move billions of dollars across global financial markets within minutes.

Some traders follow these signals closely, position themselves accordingly, and make money from volatility that others fear.

And if someone somehow knows what is likely to happen before everyone else, their profits can become extraordinary.

The oldest advantage in markets remains unchanged.

Information travels.

But it rarely travels equally.

The Final Verdict

So, who won the West Asia war?

The answer depends on what metric is being used.

If the metric is territory, military objectives, or political leverage, historians will debate it for years.

If the metric is human welfare, everyone lost.

Families lost loved ones. Countries lost economic stability. Consumers lost purchasing power. Investors lost peace of mind. Governments lost fiscal flexibility. And millions of ordinary people paid a price for decisions they never participated in making.

The winners were not necessarily nations. The winners were those standing on the right side of the economic consequences. The winners were reconstruction companies and contractors and indirectly the countries they belong to. The winners were disciplined investors who stayed invested through the uncertainty. The winners were those positioned to benefit from volatility rather than fear it. That is perhaps the uncomfortable truth about modern conflicts.

Wars are often presented as battles between countries. In reality, they are frequently transfers of wealth, opportunity, and risk between different groups of people.

The ordinary citizen bears the cost. The system reallocates the rewards. And by the time the world begins discussing who won and who lost, the bill has already been paid.

Ultimately, this conflict forces us to re-examine the popular belief that nobody wins a war. For millions of families, taxpayers, consumers, and workers across the world, that statement remains painfully true. Yet history shows that every war creates a different class of beneficiaries – those positioned to profit from reconstruction, volatility, information, or political leverage.

Perhaps that is the most uncomfortable lesson of all.

Wars rarely create wealth; they redistribute pain broadly and rewards selectively.

Disclaimer: This article is published by Ara Financial Services Pvt. Ltd. (ARN-76035), an AMFI-registered Mutual Fund Distributor, for investor education and general informational purposes only. It is not investment advice or a recommendation to buy, sell or hold any investment product. Mutual Fund investments are subject to market risks, read all scheme related documents carefully. Please consult your financial and tax advisors before making any investment decision.

Shreedhara is the Founder & Director of Ara Financial Services Pvt. Ltd. He has an experience of over 2 decades in Financial Service Industry with majority of it in guiding individuals and institutions on their investments requirements.

1 thought on “Who Really Won the West Asia War? The Hidden Winners and Losers of Conflict”

I was expecting a normal financial view. Very pleasantly surprised and happy to see such thoughtful views.

The focus on life and impact of some random external decisions on an individual was very well brought out.

Kudos, Sridhar !!